<meta name="google-site-verification" content="0S72xkYcSqqt100ZuIzn_Zif1zL8vIvcXUmc5Tjo10o" />

In a nutshell? Metallic silver, often overlooked, is a strategic halal asset in 2025, combining material security and spiritual anchorage. It combines wealth preservation and Sharia compliance, with a variety of certified investment methods. Symbolizing the Sunnah of the Prophet and the historic Dirham, it embodies the union of faith and responsible finance in an uncertain economic climate.

Many people looking for a halal silver investment in 2025 are unaware that this metal represents a unique opportunity, combining spiritual value with a sound economic strategy. Often overshadowed by gold, silver, historically used as a dirham and blessed by the Sunnah, has established itself as a tangible asset, in line with Islamic principles (no riba, gharar or maysir). Discover how, against a backdrop of uncertainty, this industrially strategic metal (electronics, medicine, renewable energies) can be used to build a blessed wealth, in line with your convictions. Combining physical security and intelligent diversification, it secures your financial future without compromising on transparency, while honoring an age-old tradition of responsible savings.

Contents

Silver and Sharia: why this precious metal is a pillar of halal investment in 2025

While gold is often the first thought for Muslim investors, what unique advantages does silver bring as a halal asset?

Faced with the economic uncertainty of 2025, marked by geopolitical tensions and persistent inflation, tangible assets are regaining their safe-haven status. Silver, a precious metal with a deep Islamic heritage, represents a strategic opportunity to align savings and spiritual values.

Unlike investments based on forbidden interest (riba) or excessive speculation (maysir), physical money or money backed by real transactions offers a Sharia-compliant solution. Namlora, the Islamic investment ecosystem, makes it a cornerstone of its approach, promoting transparency, justice and wealth preservation.

"Investing in silver means choosing an asset that is both rooted in our history and focused on the future, a way of preserving one's heritage while honoring one's faith."

In 2025, this precious metal symbolizes much more than just a financial opportunity. It represents an investment ethic in which every transaction reflects the principles of faith, responsibility and sustainability dear to Islamic finance. This reflection opens the door to concrete solutions for halal investing, balancing material return with spiritual conformity.

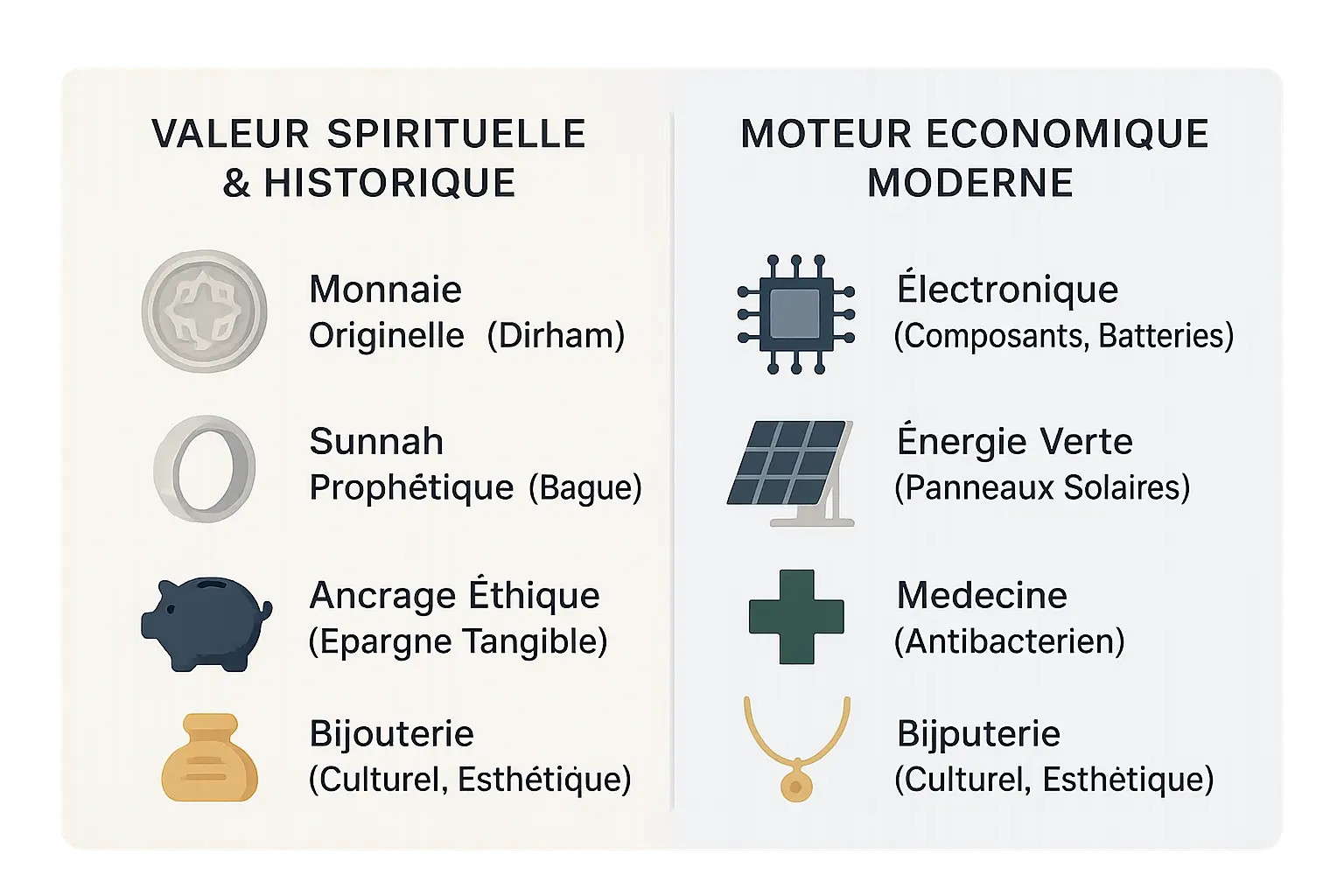

The dual value of money in Islam: a spiritual treasure and an economic engine

A currency rooted in history and faith

Silver is not just a metal: it is deeply rooted in the history of Islam.

- Historical currency: The silver dirham was the official currency of the Muslim world for centuries. Issued as early as the reign of Abd al-Malik, it bore religious inscriptions and ensured fair exchanges. This monetary system lasted until the XIXᵉ century, as evidenced by the use of dirhams in Morocco before the adoption of the franc under the French protectorate.

- Sunnah symbol: The Prophet Muhammad ﷺ wore a silver ring, legitimizing its use for men - a rare exception to the prohibitions on male jewelry. This practice symbolizes the balance between simplicity and an element of distinction.

- Tangible ethics: unlike modern monetary systems, physical money embodies transparency. Its real possession reduces the risk of financial exploitation, in line with Islamic principles. Transactions in dirhams avoid the abuses associated with riba, as they are based on a tangible asset.

A metal at the heart of the modern economy

Silver remains strategic in the key sectors of the XXIᵉ century.

In technology, it's a must-have. Smartphone circuit boards, 5G antennas and solar panels all use its exceptional conductivity. Each electric vehicle contains between 25 and 50g of silver, far more than thermal cars. Lithium-silver batteries, though rare, offer superior energy density.

In medicine, silver-based dressings fight infection, while medical implants incorporate the metal for its natural sterility. Surgical scalpels and forceps are sometimes coated with silver for their bacterial resistance. Its antibacterial properties are even being explored to combat antibiotic resistance.

Unlike gold, which is forbidden to men, silver is freely integrated into jewelry, particularly in Muslim cultures. Silver directories, a legacy of the Sunnah, remain highly prized throughout the Arab world. Historic dirhams are even collected as cultural symbols.

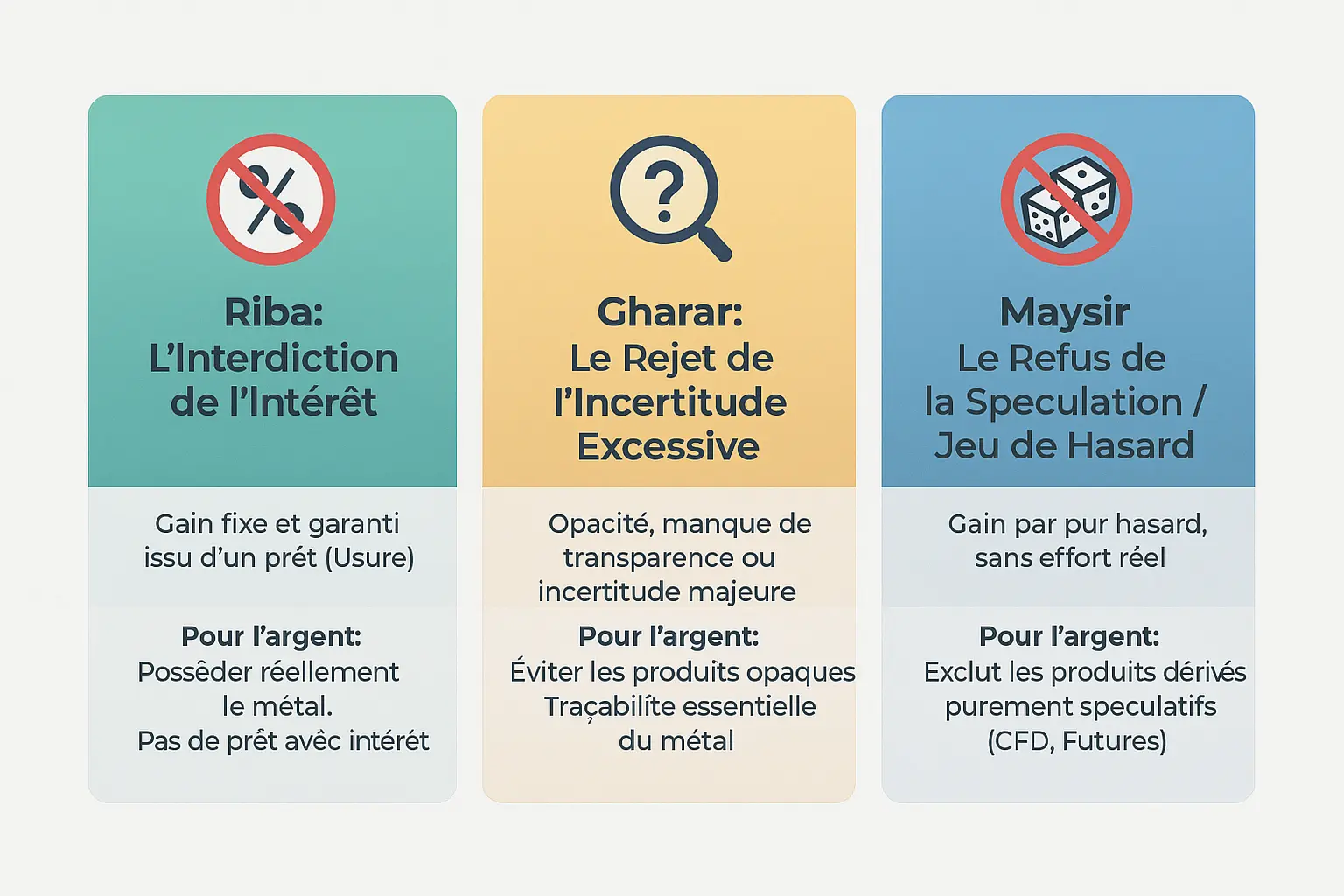

The 3 pillars of Islamic finance: the ethical framework for your money investment

Investing in money with a halal approach means adhering to an ecosystem of ethical values. Islamic finance is based on three key principles: the prohibition of Riba (interest), the rejection of Gharar (excessive uncertainty) and the rejection of Maysir (speculation). These rules transform money into a lever for economic justice, as advocated by Namlora, a halal investment ecosystem aligned with Islamic values.

The prohibition of Riba: compulsory physical possession

Riba refers to any guaranteed gain without shared effort or risk. In Islamic finance, this prohibits income from interest-bearing loans. For silver, it requires physical possession of the metal. Interest cannot be earned via conventional savings accounts. Halal assets include certified bullion or ETCs backed by real metal, such as Sprott's P-ETCs, stored in secure deposits.

Gharar rejection: the need for traceability

The Gharar prohibits opaque investments. Money must be stored in certified vaults, with regular audits. Shariah certification guarantees the metal's real presence in secure deposits such as those held by the Banque de France or the US Federal Reserve. Investors must demand documents proving the metal's physical existence, avoiding unbacked virtual certificates.

Maysir's refusal: eliminating speculation

Maysir prohibits effortless gains, such as CFDs or unbacked futures contracts. These tools transform money into a betting instrument, contrary to Islamic values. Halal mechanisms include Murabaha, where the bank buys the asset and then resells it at a specified margin, and Sukuk, Islamic securities representing a share of ownership in an asset. Speculation is thus replaced by concrete transactions.

By respecting these pillars, money becomes an ethical asset, a symbol of trust between investors. Namlora reflects this vision, structuring a Sharia-compliant investment ecosystem while promoting transparency and accountability.

How to invest in halal money: 3 concrete methods and their particularities

1. L’achat physique : Lingots et pièces (le Dirham moderne)

L’achat d’argent physique reste la méthode la plus alignée avec les principes islamiques. En détenant des lingots ou des dirhams certifiés, vous éliminez tout risque de riba ou de gharar. Des institutions comme Lina Finance proposent des dirhams frappés selon des critères Shariah, garantissant un investissement concret et éthique.

Le stockage sécurisé coûte 0,84% annuel de la valeur stockée, avec des frais fixes de 19€ pour l’ajout ou le retrait. La liquidité est limitée comparée aux produits financiers cotés, mais la possession physique rassure les investisseurs soucieux de transparence. Par exemple, 5 000€ d’argent nécessitent un budget de 3,5€ par mois pour le stockage. Pour 100 000€, le coût atteint 70€ mensuels, avec une assurance incluse dans l’offre.

2. Les ETC/ETP adossés physiquement

Les ETC/ETP (Exchange Traded Commodities/Products) offrent une alternative moderne. Chaque unité représente une quantité précise d’argent stocké dans des coffres certifiés. Leur liquidité est optimale : vous les achetez et vendez comme des actions via un courtier, sans gestion logistique. Des plateformes comme Bybit proposent des ETC certifiés halal, supervisés par des experts en finance islamique via CryptoHalal et Zico.

Pour garantir la conformité, vérifiez la certification Sharia via des organismes reconnus (ex. AAOIFI). Ces produits combinent accessibilité numérique et éthique islamique, avec des frais de gestion entre 0,40% et 0,79% annuels. Les ETF comme iShares MSCI USA Islamic UCITS (0,30% de frais) ou HANetf Saturna Al-Kawthar (0,75% de frais) illustrent des options certifiées.

3. Le contrat Murabaha sur métaux précieux

Le Murabaha, pratiqué par des banques islamiques comme Al Rayan Bank ou Chaabi Bank, permet d’acquérir de l’argent via un contrat de vente à crédit. La banque achète le métal puis vous le revend avec une marge prévue. Ce mécanisme élimine le riba tout en simplifiant le processus. Par exemple, Chaabi Bank propose des financements sur 20 ans avec un apport minimal de 10%.

Comparez les marges appliquées : certaines banques proposent des taux compétitifs pour attirer les épargnants. La transparence du contrat reste essentielle pour éviter les abus. Ce type de contrat illustre pourquoi les banques islamiques sont différentes des banques traditionnelles, en intégrant les valeurs de la finance islamique. Des acteurs comme Mizen ou 570easi développent aussi des solutions digitales pour faciliter ces transactions.

Comparison of halal silver investment methods

| Method | Level of Sharia compliance | Benefits | Points to watch |

|---|---|---|---|

| Physical purchase | Very high (direct ownership) | Full control, tangible assets, no financial intermediaries | Storage, insurance, reduced liquidity |

| FTE/physical FTE | High (if certified) | Liquidity, no logistics management | Sharia certification required, management fees |

| Murabaha | High (Islamic structure) | Offered by Islamic banks, no storage | Variable margin, contract transparency |

| Derivatives - CFDs, Futures | No conformity | N/A | Based on speculation and uncertainty. To be avoided. |

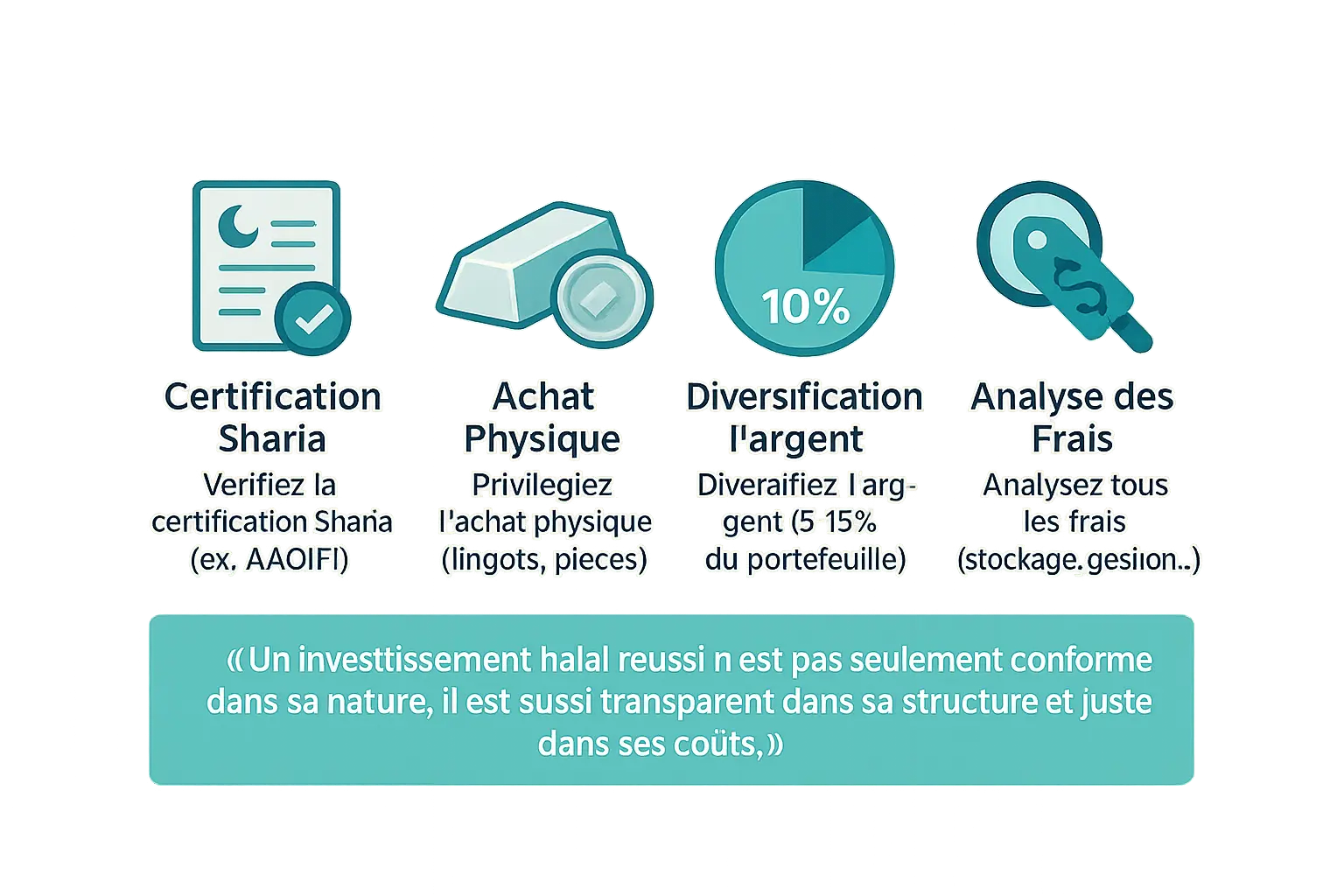

Points to watch for a safe and compliant silver investment

Investir dans l’argent halal exige une vigilance rigoureuse. La certification Shariah constitue le socle de toute opération responsable. L’AAOIFI, autorité de référence en finance islamique, édicte des normes techniques pour valider la conformité des actifs. Exigez toujours un certificat authentique avant d’acquérir un produit.

- Check certification: Demand a Sharia certificate for ETCs and funds, issued by recognized bodies such as AAOIFI.

- Focus on the tangible: ingots and physical coins remain the benchmark for avoiding the risks associated with unbacked derivatives.

- Diversify wisely: Silver can make up 5-15% of a balanced portfolio, combined with halal real estate or ethical equities.

- Analyze costs: Identify all costs (purchase, storage, management, sale). Annual storage costs vary according to the value held, with examples of variable costs.

"A successful halal investment is not only compliant, it's transparent in its structure and fair in its costs."

Diversification remains essential to spread risk. By combining silver with other assets, such as halal real estate, you can build a portfolio while securing your savings.

Hidden costs deserve special attention. Physical bullion storage generates variable costs. ETCs require an analysis of fees calculated as a percentage of the value held, often between 0.49% and 1.50% per annum.

In 2025, silver is more than a metal: it's a choice of conviction

Investing in halal silver means choosing a tangible, affordable asset rooted in Islamic tradition. This precious metal embodies a dual spiritual and economic value, in accordance with Sharia principles.

L’interdiction du riba, du gharar et du maysir guide chaque décision d’investissement. En privilégiant des solutions comme les lingots physiques, les ETC certifiés ou les contrats Murabaha, l’investisseur musulman construit un patrimoine durable et béni.

Money recalls the heritage of the dirhams used in the prophetic economy. It enables us tohonor our faith while preserving our financial freedom, far from speculative mechanisms.

The Namlora ecosystem supports this choice of conviction. It offers tools to help you invest in line with your values, while contributing to a fair and transparent business model.

In 2025, money remains a pillar of Islamic investment. It symbolizes the fusion of financial responsibility and fidelity to Islamic teachings.

In 2025, investing in halal money is a choice of conviction, combining sustainable heritage and the honor of faith. A tangible asset historically rooted in Islam, it allows us to preserve its wealth while respecting the pillars of Sharia law. Opt for finance aligned with your values and discover safe, ethical investment solutions via Namlora.

FAQ

Where can I invest my money halal in 2025?

L’investissement halal en argent physique reste une option solide pour les musulmans souhaitant allier foi et finance. Les méthodes les plus conformes incluent l’achat de lingots ou de dirhams modernes, des ETC/ETP adossés à l’or gris ou à l’argent (avec certification Shariah) et les contrats Murabaha. Ces solutions évitent le Riba (intérêt), le Gharar (incertitude) et le Maysir (spéculation), piliers de la finance islamique. Privilégiez des actifs tangibles et vérifiez toujours les certifications pour éviter les produits opaques.

Pour une approche équilibrée, l’argent peut représenter 5 à 15 % de votre portefeuille, complétant d’autres placements comme l’immobilier halal ou des ETF conformes. Attention aux frais cachés (stockage, commissions) et diversifiez raisonnablement pour réduire les risques tout en préservant votre tranquillité d’esprit.

Is investing money Sharia-compliant?

Oui, l’investissement est halal tant qu’il respecte les principes islamiques. L’argent, en tant que métal précieux, incarne cette éthique : il est permis aux hommes (contrairement à l’or) et son usage est ancré dans la Sunnah. Cependant, la méthode compte. Évitez les produits dérivés (CFD, futures) ou les comptes bancaires générateurs d’intérêt. Optez plutôt pour l’achat physique, des ETC certifiés ou des contrats Murabaha, où la banque achète l’actif puis vous le revend avec une marge transparente. La clé ? La possession réelle de l’actif et la transparence des frais.

En 2025, l’argent reste un choix stratégique : son utilisation industrielle (panneaux solaires, électronique) renforce sa valeur à long terme, tout en s’alignant sur une vision durable et spirituelle de la gestion de patrimoine.

Is investing money haram?

Non, l’investissement n’est pas haram tant qu’il respecte les enseignements de la Sharia. Ce sont les méthodes qui peuvent l’être : par exemple, prêter à intérêt (Riba), spéculer sans possession réelle (Maysir) ou acheter des produits opaques (Gharar). L’argent, en revanche, est un actif tangible et éthique. Sa conformité est maximale lorsqu’il est détenu physiquement (lingots, bijoux) ou via des structures certifiées. Ainsi, votre épargne prévoit l’avenir sans éloigner votre foi.

Le Prophète ﷺ portait une bague en argent, illustrant son acceptabilité. C’est une opportunité pour les musulmans de construire un patrimoine béni, en s’appuyant sur des mécanismes clairs et des preuves de stockage, tout en évitant les pièges des marchés spéculatifs.

What are the most profitable halal investments at the moment?

L’argent physique et les ETF adossés à l’or ou à l’argent certifié Shariah figurent parmi les placements les plus solides. Leur valeur est soutenue par des usages industriels croissants (médical, énergie solaire) et leur rôle historique de réserve de valeur. Les contrats Murabaha, bien que moins liquides, offrent une alternative bancaire sans Riba. En 2025, ces actifs se distinguent par leur accessibilité et leur alignement avec les principes islamiques.

Pour maximiser le rendement, diversifiez raisonnablement : l’argent peut compléter des ETF halal (comme SPUS ou HLAL) ou des sukuk. Cependant, évitez les produits complexes à effet de levier ou les marchés à terme, jugés non conformes. La rentabilité durable s’obtient par la patience et la vérification des certifications, pas par la spéculation.

How to earn halal money fast?

En finance islamique, la rapidité va de pair avec la prudence. L’argent physique, bien que tangible, n’est pas un placement à court terme. Pour des gains plus rapides, concentrez-vous sur des revenus actifs (emploi conforme, commerce) ou des investissements à court terme comme les sukuk à court terme, mais vérifiez leur structure pour éviter le Riba. Les ETC certifiés peuvent offrir une liquidité accrue, mais évitez les CFD ou les futures, qui incarnent le Maysir.

Rappelez-vous : l’islam valorise l’épargne responsable. L’argent, souvent utilisé comme épargne familiale via des dirhams, symbolise cette sagesse. Pour un rendement rapide et halal, priorisez les opportunités locales, comme le commerce de biens physiques, tout en gardant un œil sur la conformité Sharia de chaque décision.

How to save without falling into Riba?

Épargner sans Riba passe par des actifs physiques ou des contrats islamiques. L’argent en lingots ou dirhams est une solution directe, mais le stockage et la liquidité peuvent être des défis. Les ETC adossés à l’argent, avec certification Shariah, offrent une alternative plus pratique. Les comptes de dépôt en banque islamique, suivant des mécanismes comme le Mudaraba (partenariat), évitent les intérêts tout en générant des revenus via des investissements réels.

Pour les débutants, commencez par des dirhams certifiés, stockés dans un coffre personnel ou via des plateformes transparentes. Les contrats Murabaha, bien que plus onéreux, permettent d’acheter des actifs sans emprunter à intérêt. Enfin, diversifiez avec des ETF halal ou des obligations sukuk pour une gestion proactive sans compromettre vos valeurs.

What type of trading is considered halal?

Le trading halal exclut toute spéculation ou prêt à intérêt. L’achat-vente d’argent physique en temps réel, sans effet de levier, est conforme. Les ETC certifiés Shariah, qui reflètent le prix du métal sans produits dérivés, sont également acceptables. En revanche, les CFD (contrats sur la différence) ou les futures, basés sur la spéculation et la possession virtuelle, sont Haram. Le trading de devises (Forex) est autorisé uniquement en mode spot (échange immédiat), sans délaissement.

Pour un trading responsable, privilégiez les plateformes certifiées et vérifiez la traçabilité des actifs. L’or et l’argent, avec leur histoire islamique, offrent une base solide pour un trading spirituellement aligné. En 2025, leur demande industrielle soutient leur volatilité modérée, idéale pour des stratégies de moyen terme.

How can I invest in real estate in a halal way?

L’immobilier halal repose sur des contrats comme le Ijara (location) ou le Diminishing Musharaka (copropriété progressive). Les banques islamiques proposent des financements via Murabaha : elles achètent le bien puis vous le revendent avec une marge, sans intérêt. Évitez les prêts conventionnels, qui incorporent du Riba, et vérifiez que les revenus locatifs proviennent de sources licites (pas d’activités interdites sur les lieux). Les ETF immobiliers halal, comme IGDA, sont une alternative indirecte mais nécessitent une certification Shariah.

Comme l’argent, l’immobilier est un actif tangible. Les deux peuvent constituer des piliers d’un portefeuille diversifié. Cependant, l’immobilier exige une gestion active, tandis que l’argent offre plus de liquidité. En 2025, les deux secteurs se complètent pour un investissement équilibré, à condition de respecter les principes islamiques à chaque étape.

Like money, real estate is a tangible asset. Both can be pillars of a diversified portfolio. However, real estate requires active management, while cash offers greater liquidity. In 2025, the two sectors complement each other for a balanced investment, provided Islamic principles are respected at every stage.