<meta name="google-site-verification" content="0S72xkYcSqqt100ZuIzn_Zif1zL8vIvcXUmc5Tjo10o" />

Key points to remember: Strategic prudence and solid legal structures, such as the holding company, transform Islamic investments into levers of Baraka. By avoiding Riba and favoring tangible assets, every ethical choice protects capital and fuels lasting social impact. The 2008 crisis proved that these principles ensure stability and resilience.

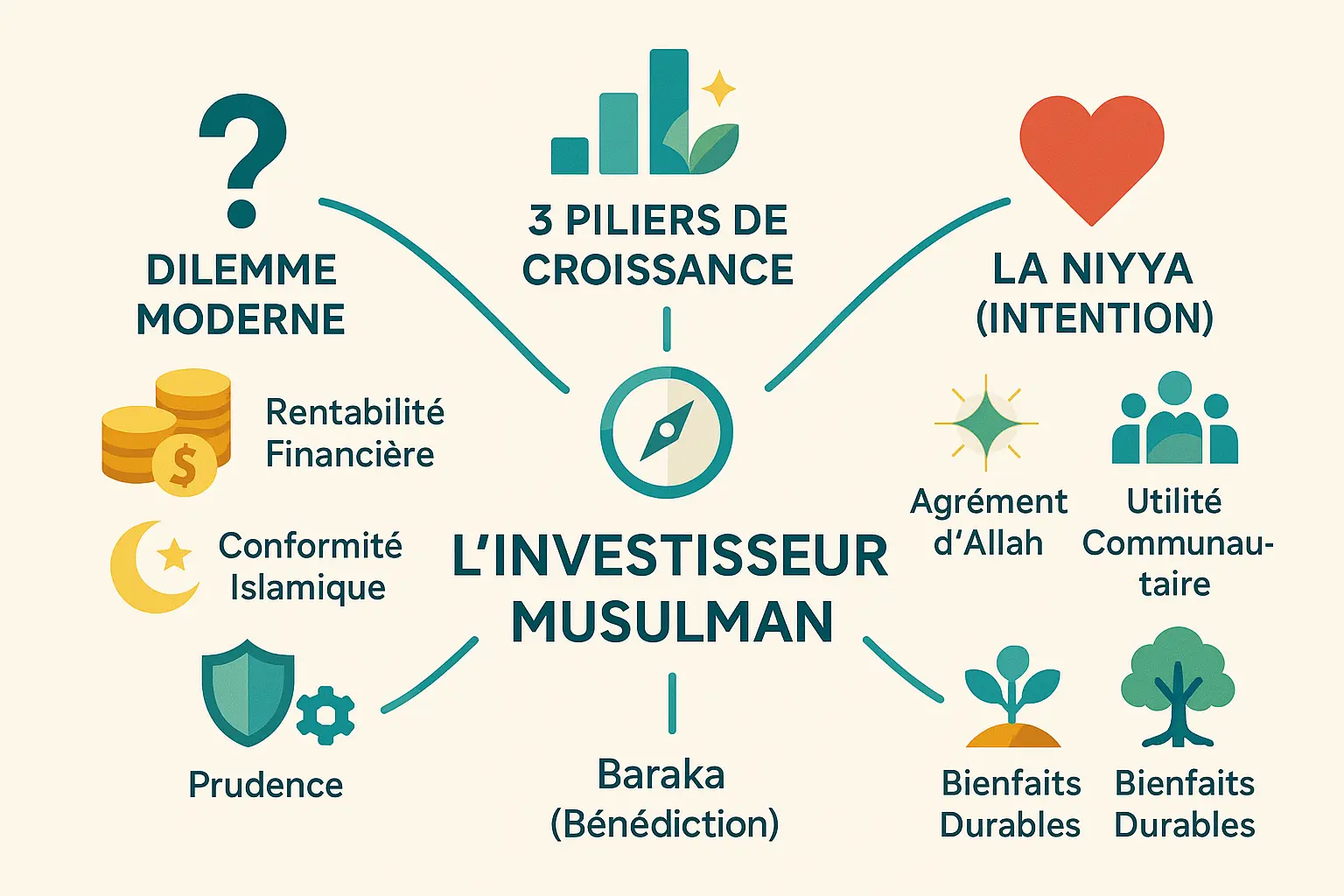

The ethics of the Muslim investor face a modern dilemma: how to reconcile profitability and Islamic compliance in a complex financial landscape, where the temptation of immediate profit can drive away spiritual values? This article explores the pillars of responsible investment - prudence, sound legal structure and sincere intent (Niyya) - to align financial choices with Sharia teachings. Discover how concrete mechanisms, such as the creation of holding companies or progressive profit-sharing clauses, transform assets into levers of stability and Baraka, avoiding the pitfalls of speculation and over-dependence.

Contents

Introduction: investing with wisdom and faith in the modern world

The investment world is moving at breakneck speed. Between fund-raising, digital businesses and real estate projects, opportunities abound. But for a committed Muslim, a crucial question arises: how do you grow your capital without compromising your values?

This guide offers you a spiritual and financial compass. We explore three pillars: prudence as an expression of your faith, legal structures as safeguards, and Baraka as the divine reward for doing business with integrity. These concepts provide a clear framework for investing in accordance with your convictions.

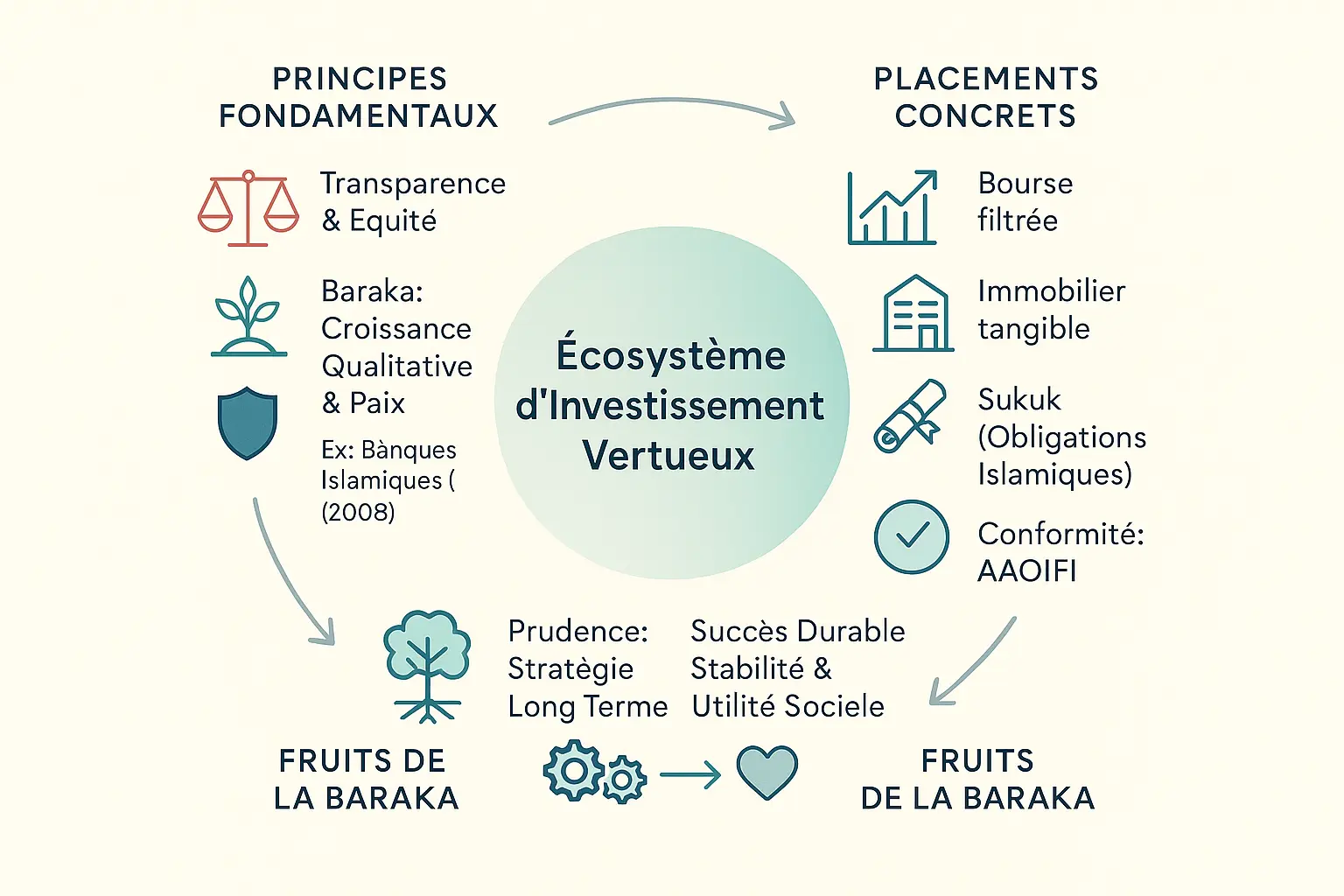

In Islam, intention (Niyya) is just as important as action. Your investments must be profitable and in line with the teachings of the Koran. It is this pure intention that paves the way for Baraka, the divine blessing that transforms your efforts into spiritual and social benefits.

Discover how to structure your investments to protect your capital and your soul, avoid the pitfalls of the financial markets, and align your decisions with ancestral wisdom to cultivate sustainable growth. Because in Islam, success is measured in impact, not just numbers.

The foundations of the Muslim investor's ethic: the essential principles

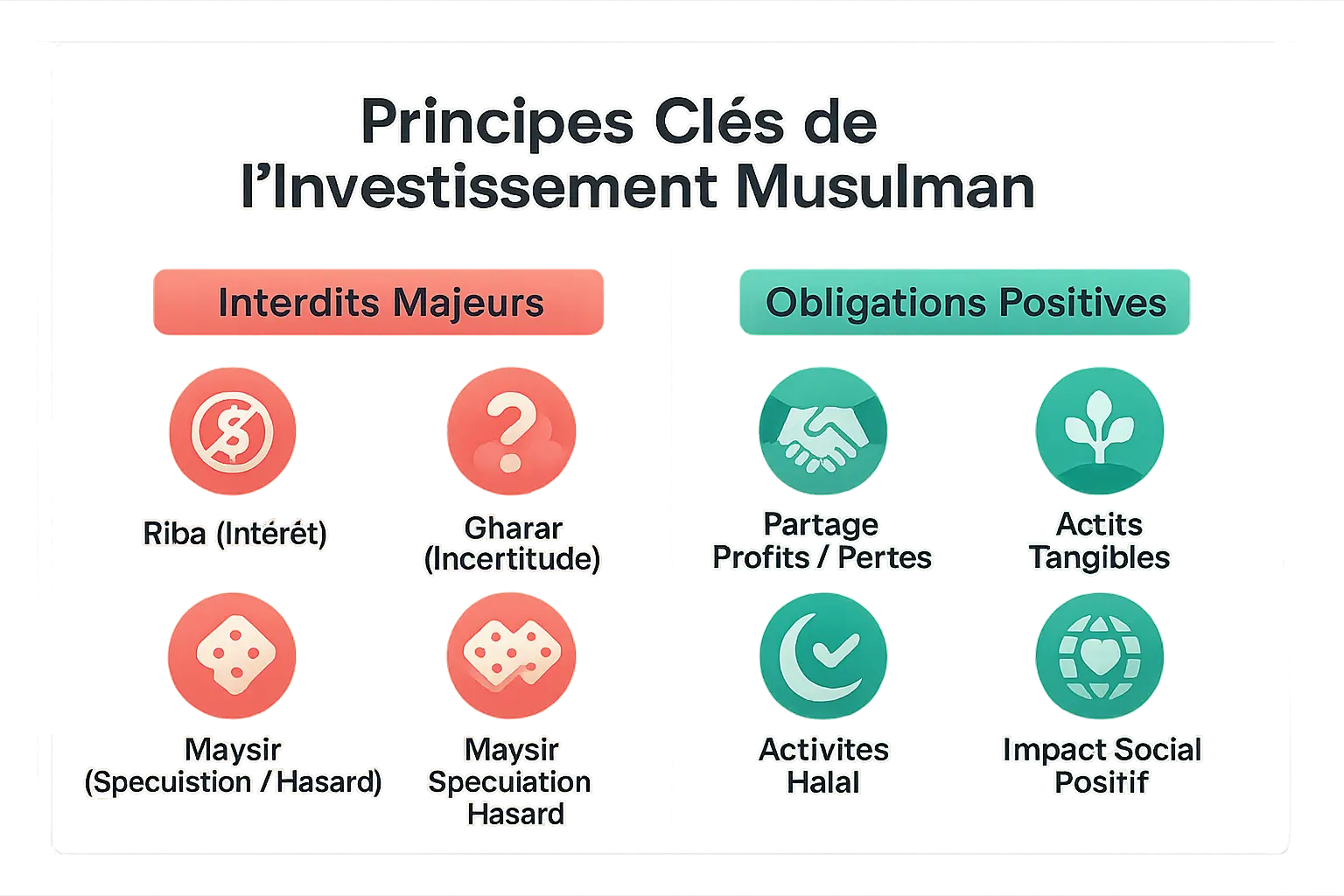

Major prohibitions as safeguards

Islamic finance regulates the pursuit of profit to guarantee fairness, ensuring that money does not become a tool of injustice. Three key principles protect individuals and society:

Riba prohibits any risk-free fixed gain. Unlike conventional loans, the remuneration depends on the actual results of the project. This rule is based on the Koran (2:278-279), which denounces usury, and Hadiths in which the Prophet describes "a dirham of Riba" as an act more serious than adultery. In practice, this excludes products such as traditional bank accounts that generate automatic interest.

Gharar rules out ambiguous contracts. A transaction must be clear and without deception, guaranteeing transparency. For example, selling fish still in the sea or unripe crops is forbidden, as it creates unpredictable risks. This rule protects the parties from uncertain agreements and limits conflicts.

The Maysir condemns random speculation. Speculation in Islam is likened to gambling without value creation, deepening inequalities. Products such as financial options or speculative cryptocurrencies, which are based on unpredictable fluctuations rather than a real economy, are prohibited.

Positive obligations for ethical investment

Beyond the prohibitions, halal investment rests on four pillars that transform money into a lever for responsible development:

- Profit and loss sharing (PLS): Entrepreneur and investor share risks and rewards, reinforcing trust. Mechanisms such as Musharakah (parceria) or Mudaraba (investor-capital) ensure equity in the financial commitment.

- Backed by real assets: As emphasized by the French Ministry of the Economy, every transaction must be based on a tangible asset (real estate, machinery, merchandise). This requirement eliminates speculative bubbles and anchors the economy in reality.

- Financing lawful activities: Money must not flow into Haram sectors (alcohol, gambling). Muslim investors apply strict criteria: a company that generates more than 5% of its revenues from non-compliant activities is excluded.

- Social responsibility: job creation, environmental protection and community support guide our decisions. Institutions such as Baraka Halal Finance co-finance social projects such as drinking water wells and agricultural cooperatives, illustrating Namlora's ethical vision.

The ethics of the Muslim investor aim to combine profitability and spiritual conformity, with a focus on fairness, transparency and positive impact on society.

Prudence in action: how to structure your investments to attract the Baraka

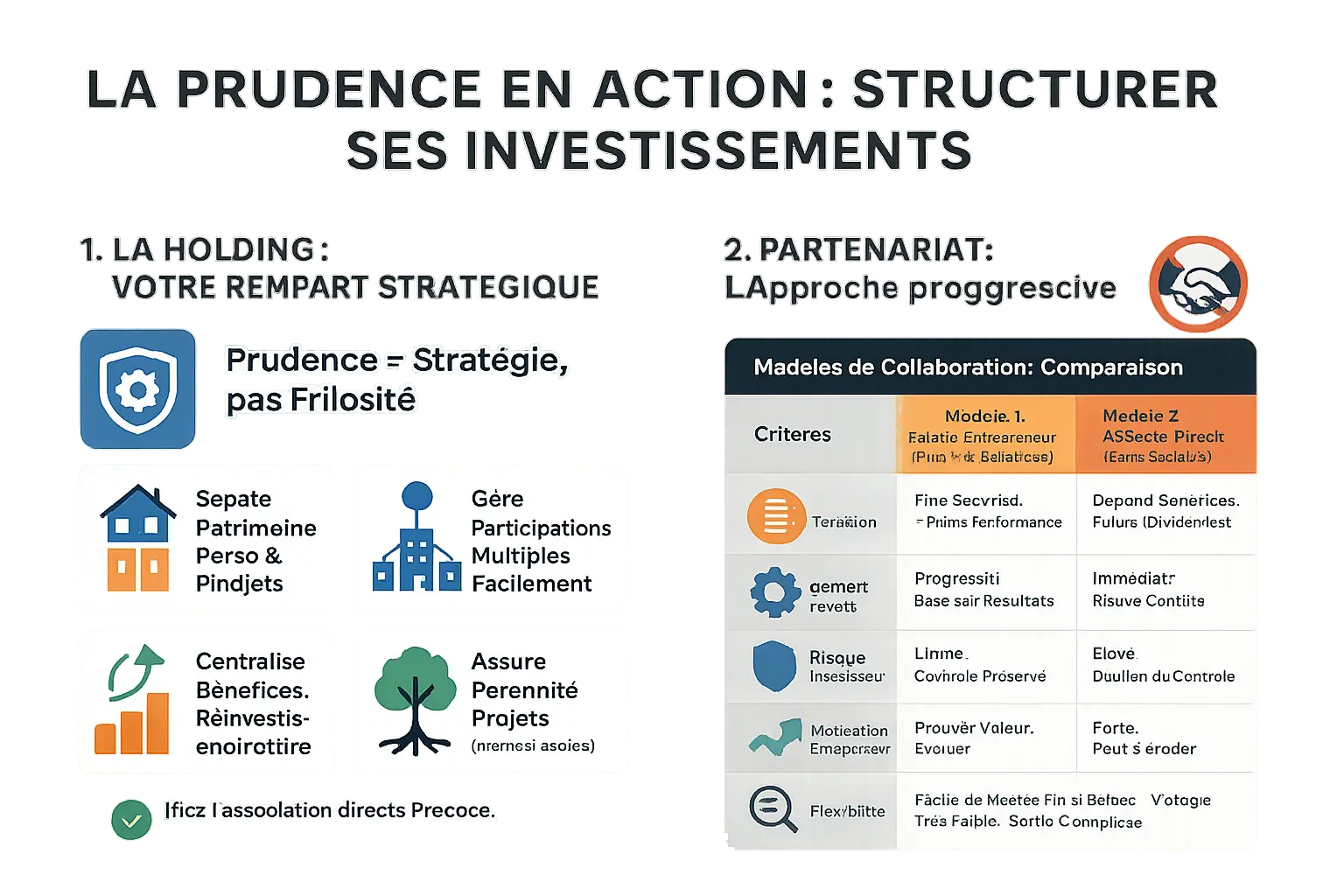

Legal structure, the investor's first line of defence

Sharia-compliant investment requires a strategic vision. The holding company protects personal assets from risk, while respecting the prohibition of Riba and Gharar. By centralizing the management of shareholdings, it guarantees the continuity of projects, even in the event of disagreement between partners. For a Muslim investor, this is an essential tool for reinvesting in ethical activities such as agricultural cooperatives or ecological projects.

Its tax advantages reinforce security: virtual exemption of dividends via the parent company-daughter regime, pooling of profits between subsidiaries. A mechanism that encourages ethical reinvestment, in line with the objective of Baraka - the divine blessing linked to righteous acts. In practical terms, this structure makes it possible to clearly separate halal profits from licit activities, thus facilitating compliance with Islamic principles.

Associating wisely: a progressive approach to partnership

Favoring an intermediate model - fixed salary + percentage of profits - before granting shares allows us to test a partner's reliability. This prudence prevents future conflicts and protects the project. It reflects the Islamic approach, which values patience and verification before final commitment.

| Criteria | Model 1 - Employee-entrepreneur (Fixed salary + % of profits) | Model 2 - Direct partner (shares) |

|---|---|---|

| Compensation | Stable remuneration + performance bonus | Depends entirely on future earnings |

| Alignment of interests | Progressive, results-based | Immediate but risk of disagreement |

| Investor risk | Preserved control | Dilution of decision-making power |

| Entrepreneurial motivation | Prove your worth and grow | Strong but unstable in difficulty |

| Flexibility | Easy to adapt if objectives not achieved | Costly exit |

This model reflects Islamic wisdom. As halal investment platform Namlora reminds us, transparency and a sustainable vision are essential to earning divine Baraka. By combining moderation and foresight, the Muslim investor builds not only a solid wealth, but also a spiritual legacy that benefits his community.

Pitfalls to avoid for a safe, compliant investment

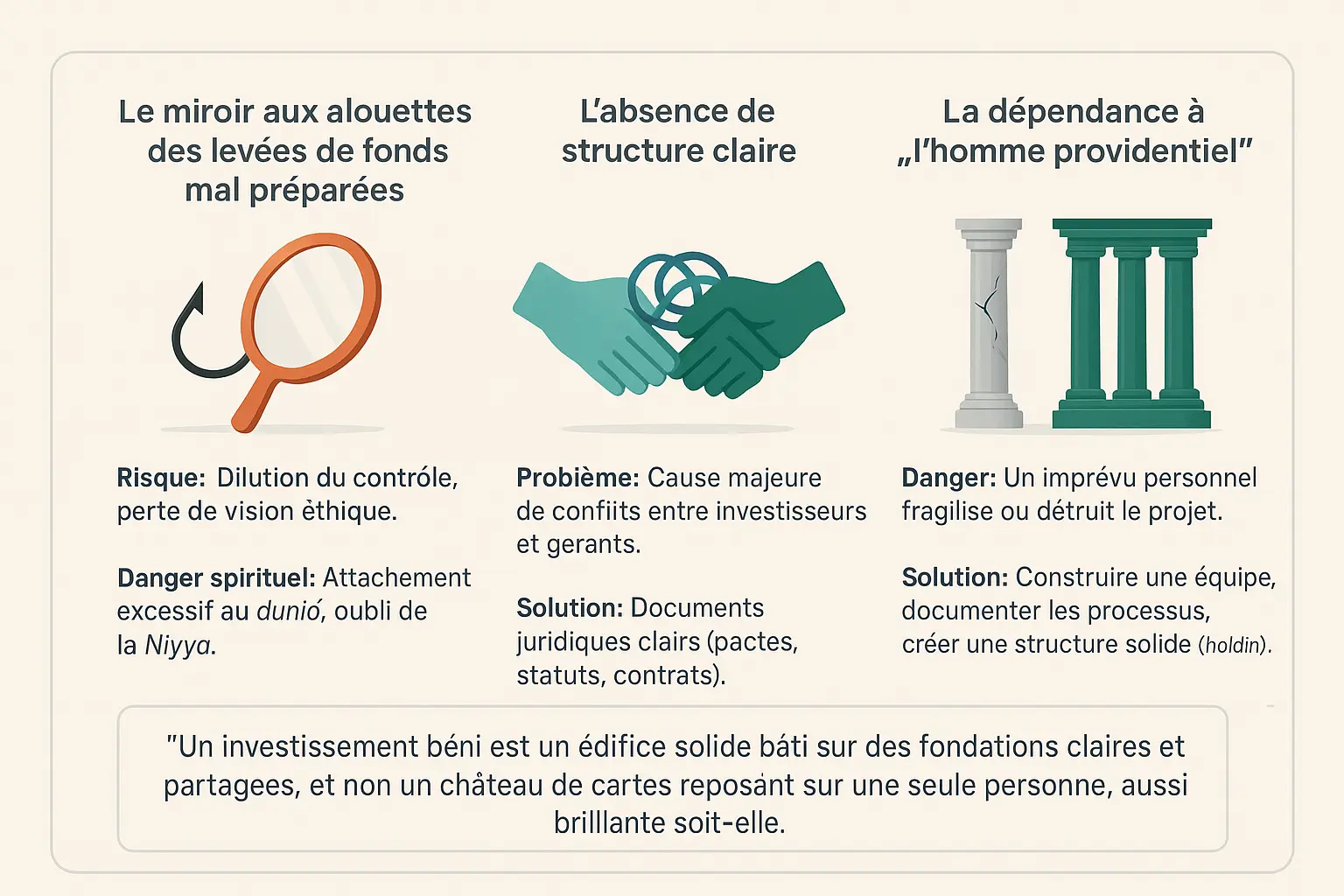

The lure of ill-prepared fund-raisers

Fund-raising, while sometimes necessary, conceals major risks. Without rigorous supervision, they dilute the control of the initial investor. This phenomenon exposes the ethical vision of the project to entrants motivated by pure profit, distancing the initiative from Islamic principles.

Sur le plan spirituel, ces levées de fonds peuvent engendrer un attachement excessif au dunia. La recherche effrénée de financement éclipsant la Niyya initiale (intention sincère) remet en cause la bénédiction divine (Baraka) dans les affaires. Une alternative existe : des plateformes comme Lina proposent des solutions éthiques, avec validation par un Conseil Shariah indépendant.

The absence of a clear structure: the royal road to conflict

An investment without a solid legal framework is like a boat without a rudder. Partnership agreements, clear articles of association and service contracts are not superfluous formalities. They avoid conflicts between investors and managers, so common in poorly structured projects.

The Islamic Development Bank illustrates this need. By incorporating conflict prevention principles (Do No Harm), it shows how clear rules protect both capital and human relationships. Without structure, trust is not enough to guarantee sustainability.

The risk of dependence on the "providential man

A project that relies on a single person, no matter how competent, is fragile. Illness, a change of life or an unforeseen personal event can put an end to the business. The solution lies in building solid teams, documenting processes and using structures such as holding companies to ensure continuity.

A successful investment is a solid edifice built on a clear, shared foundation, not a house of cards resting on a single person, no matter how brilliant.

Key man insurance, used in tech companies, illustrates this principle. It compensates for the loss of a key employee, preserves stability and reflects the spirit of solidarity typical of Islamic investment.

Building a virtuous investment ecosystem: from prudence to Baraka

Transparency and fairness: the seeds of Baraka

Baraka embodies a divine blessing that transcends material wealth. It manifests itself in financial stability, inner peace and positive social impact. This blessing is attracted by ethical practices. Total transparency in the management and distribution of profits is essential. Fairness guides transactions, as demonstrated by the resilience of Islamic banks during the 2008 crisis. Their model, based on tangible assets and profit/loss sharing, has protected them from toxic products. Their low leverage and refusal to speculate prevented the collapses seen in the conventional banking system.

Concrete investments for real impact

L’investissement en bourse s’adapte aux filtres éthiques, excluant alcool, jeux et favorisant les entreprises saines. Pour bien débuter, maîtrisez les bases de l’investissement islamique. Par exemple, des outils comme les ETF halal certifiés par des comités de Shari’ah permettent d’éviter les secteurs prohibés tout en diversifiant les risques.

Real estate, a tangible asset, requires clear compliance. Rents and financing must respect fair principles, avoiding interest rates. To find out more, consult the opinions of scholars on real estate. A concrete example: a halal real estate investment fund can finance social housing, generating rental income without resorting to usury.

Sukuk, Islamic bonds backed by real assets, avoid speculation. Unlike conventional bonds, they represent a share of ownership in a project, with income linked to its performance. For example, a Sukuk al-Ijara can finance a solar farm, with investors receiving income from the rental of solar panels.

To ensure compliance, AAOIFI harmonizes Shari'ah standards. Understanding the differences with the Majmaʿ al-Fiqh reinforces rigor. AAOIFI sets precise criteria for judging the compliance of Sukuk or Islamic financial products, avoiding drift.

Conclusion: prudence, a strategy for lasting success

L’éthique de l’investisseur musulman transforme la prudence en force. Elle protège le capital et intègre une vision spirituelle. La réussite se mesure en stabilité, utilité sociale et conformité. La Baraka s’ancre ainsi durablement, reliant richesse et responsabilité. Aligner ses choix sur la Charia construit un héritage vertueux. Un investissement éthique nourrit la confiance, renforce les communautés et cultive une réussite alignée avec les valeurs islamiques.

C’est par cette cohérence que l’épargne devient un levier de transformation sociale.

Investir avec prudence, structurer ses projets et rechercher la Baraka permettent à l’investisseur musulman de concilier rentabilité et éthique islamique. Cette démarche, fondée sur la transparence et l’équité, transforme les finances en levier de développement durable, où succès matériel et impact social s’harmonisent pour honorer la Niyya et cultiver un héritage bénéfique.

FAQ

What is Islam's vision of investment?

L’Islam n’interdit pas l’investissement, mais il l’encadre pour garantir une croissance spirituelle et matérielle. La recherche du profit est permise à condition qu’elle respecte des principes éthiques : interdiction de l’intérêt (Riba), partage des risques (PLS) et investissement dans des activités licites (Halal). Comme un cultivateur qui plante sa semence avec soin, l’investisseur musulman doit semer son capital en respectant ces règles, pour récolter une Baraka durable, à la fois économique et spirituelle.

Par exemple, la création d’une holding permet de structurer les investissements, protégeant les parties prenantes tout en alignant la vision à long terme. C’est cette prudence qui transforme un simple projet en héritage bénit.

What is an Islamic-compliant investor?

Un investisseur halal est avant tout un penseur de long terme, guidé par une intention sincère (Niyya) et un souci de justice. Il évite les pièges comme l’intérêt usuraire ou la spéculation excessive, préférant des actifs tangibles (immobilier, entreprises vertueuses) et des partenariats équitables. Sa démarche ressemble à la construction d’un édifice : chaque décision est une pierre posée avec soin, pour assurer solidité et stabilité.

Par exemple, il privilégie des modèles progressifs (salaire fixe + part des bénéfices) avant de confier des parts sociales, testant ainsi la fiabilité de ses associés. C’est une approche qui allie confiance et pragmatisme, comme le rappelle le proverbe : « La prudence est un trésor précieux. »

What are the key principles of Islamic finance?

inq piliers forment la colonne vertébrale de la finance islamique :

L’interdiction du Riba : pas d’intérêt garanti, mais un partage des bénéfices et des pertes entre les parties.

L’actif tangible : chaque investissement doit être lié à un bien réel, comme un bien immobilier ou une entreprise productive.

Éviter l’excès d’incertitude (Gharar) : les contrats doivent être clairs, sans clauses floues ou trompeuses.

Refuser le Maysir : pas de spéculation ou de gains faciles, mais des placements basés sur l’analyse et l’effort.

Financer le licite : exclusion des secteurs Haram comme l’alcool ou le jeu.

Ces principes guident l’investisseur comme une boussole, l’aidant à naviguer vers une prospérité durable et éthique.

Does investing via Fair Invest comply with Islamic ethics?

Pour qu’un fonds comme Fair Invest soit halal, il doit respecter trois critères majeurs : une supervision par un comité religieux (Sharia Board), une transparence sur les secteurs investis (exclusion des activités Haram), et un modèle économique sans intérêt. Imaginez un jardin où chaque plante est soigneusement sélectionnée pour sa qualité : de même, un fonds islamique doit filtrer ses investissements pour cultiver une croissance bénie.

Un tel fonds pourrait financer des projets éco-responsables ou des PME locales, en s’assurant que chaque dirham investi nourrit non seulement le portefeuille, mais aussi la société. La prudence ici n’est pas une entrave, mais la garantie d’un rendement spirituel et financier.

What types of investment are prohibited in Islam?

L’investissement Haram inclut tout ce qui transgresse les enseignements du Coran et de la Sounna. Cela concerne les secteurs comme la production d’alcool, le commerce de la viande de porc, les jeux de hasard, les armes non éthiques, ou encore les banques traditionnelles basées sur l’intérêt. Une analogie simple : comme un fruit véreux peut gâter une corbeille entière, un investissement non conforme menace l’intégrité de votre patrimoine.

Évitez aussi les placements spéculatifs (ex. options binaires) ou les contrats pleins d’incertitude (Gharar), car ils ressemblent à un pari plus qu’à un partenariat. Enfin, les dettes toxiques à taux exponentiels sont à fuir comme un navire en perdition.

What are the pillars of sound Islamic finance?

La finance islamique repose sur des fondations inébranlables :

Équité : Les profits et les pertes se partagent entre investisseurs et gestionnaires, comme deux agriculteurs qui récoltent ensemble les fruits d’un champ.

Transparence : Chaque contrat est une vitrine où les clauses sont visibles, éliminant les zones d’ombre du Gharar.

Impact social : L’investissement doit nourrir la communauté, en créant des emplois ou en soutenant des innovations vertueuses.

Adhésion aux principes de la Charia : Un comité de savants veille à la conformité, comme un architecte qui vérifie que chaque poutre porte le poids requis.

Durabilité : La Baraka naît de la patience, non de la précipitation. Un projet bien structuré (via une holding, par exemple) assure sa pérennité face aux tempêtes.

Is investing in the stock market permissible in Islam?

Oui, mais avec discernement. La bourse devient haram si elle nourrit la spéculation (Maysir) ou finance des secteurs interdits (alcool, jeux en ligne). À l’inverse, elle est halal lorsqu’elle soutient des entreprises vertueuses, comme un verger qui ne cultive que des fruits sains. Par exemple, un portefeuille boursier conforme privilégie les entreprises dont les revenus proviennent à 100% d’activités licites et dont l’endettement reste modéré.

Un outil pratique : les filtres Sharia, qui éliminent les entreprises non conformes. C’est comme passer un tamis fin pour ne garder que le grain de blé, éliminant l’ivraie des investissements toxiques.

How to invest in real estate while respecting Islamic rules?

L’immobilier est un pilier de la finance halal, car il repose sur un actif tangible. Pour rester conforme, évitez les prêts à intérêt et préférez des modèles comme l’Ijara (location-vente) ou le partenariat (Moudaraba). Imaginez un partenariat où vous achetez un bien avec un associé, et vous partagez les loyers et la valeur de revente selon vos apports initaux.

Autre astuce : utilisez des structures comme la Wakala, où un gestionnaire expert gère vos biens en échange d’une rémunération proportionnelle aux profits générés. C’est un peu comme confier vos oliviers à un arboriculteur expérimenté, en échange d’une part de l’huile produite.

Why can trading be considered legal?

Le trading n’est pas interdit s’il respecte les règles islamiques : il doit porter sur des biens licites, éviter la spéculation excessive (Maysir) et reposer sur une analyse solide. Le commerce de marchandises (comme l’or ou les matières premières) ou l’achat d’actions d’entreprises vertueuses sont des exemples de trading halal. C’est un peu comme le travail d’un artisan qui transforme la matière brute en un objet utile, contrairement au joueur qui mise tout sur un lancé de dés.

Cependant, le trading à très court terme (day trading) ou les contrats à terme (futures) sont à éviter s’ils reposent sur la spéculation. La prudence ici est une vertu : mieux vaut cultiver un arbre fruitier que de chercher des trésors dans un champ de mines.